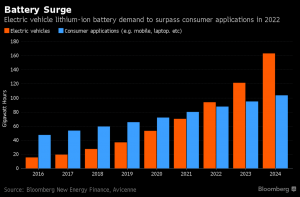

So the world is going crazy about lithium and it all sort of started back in 2015, when the price tripled (I wrote about it before). Unless you live under a rock you are very aware of this. Most projections strongly suggest that this trend will continue because the fundamentals behind these estimations are very solid; we buy more and more devices that use Li-ion batteries and the rate of growth, especially of the largest of those devices -i.e. buses and cars- is speeding up. Lithium is one of the components of these batteries, alongside cobalt, nickel to name a few.

If you have never invested in lithium companies, but are getting really curious about this sector, then this post is for you. These are the very basics that any institutional investor would know and use to evaluate companies and it’d be great if you do too. So here goes…

5 things to know before investing in lithium stocks

Before you buy a single share of a lithium focused company, you need to know that:

- Not all lithium is “created” equal. There are two main sources of lithium. You can find lithium in brine (where lithium is dissolved in subsurface water, located under the saline crust of a salt flat) or in rock, in minerals such as spodumene. And why does it matters which one? Keep reading!

- Brine is an explorer’s dream come true. It can be markedly easier to find lithium in brine, shortening the exploration process dramatically and at the same time making it less expensive. As a company exploring for lithium, your first clue in this path is, -you probably guessed this from #1- finding a salt pan. Of course, then you have to find out if there is actually a body of water underneath it, and if this brine contains lithium in an economically viable concentration. At this point, the lower limit used -equivalent to cut-off grade in a mine- is 250mg per litre. Putting a brine deposit into production is more of a chemical processing operation than a mine, so you will see a difference in the management selected to take the project forward, very soon after confirming the project’s potential.

- Hard rock has its perks too. On the other side, hard rock lithium deposits can be put into production quicker, and the investment required is normally much lower, being a more straightforward mining operation. So if the company you are analysing has found a hard rock deposit, you can expect that they may need smaller capital raises, hence causing less dilution to current investors, than a comparable company promoting a brine deposit.

- Location, location, location – key even here. Most of the global lithium resources* -67%- is located in only one region, the so-called Lithium Triangle, an area of northern Argentina, Chile and southern Bolivia. So even though Australia, Canada, and China are key players, if you want to position yourself well in this sector, you need to be exposed to South America. Or pick a company that has at least partial exposure to it.

- Buyers wanted, really. The price for lithium is defined party to party, with contracts – so this means there is no central exchange and the price is a bit more opaque for the general public. Because of this, you will see most companies that are nearing a DFS (definitive feasibility study), to be entering into off-take agreements with one or more buyers, agreeing on a price for future delivery. You will see these contracts be for either lithium carbonate or lithium hydroxide, and these may help either fund a portion of the construction or act as collateral in securing debt for project finance.

So that’s it. These are my 5 things to know before investing in lithium stocks, or “Lithium Investing 101” for you. This is a very exciting sector that has the potential to grow exponentially, so I believe it should be in everyone’s portfolio at least in some proportion. But always remember to do your own research, diversify and monitor your investments for any changes in fundamentals.

Happy investing!

P

PS: Talk to me on Twitter – @paola_rojas

*Resources do not take into account whether the minerals can be put into production at profit for the investor. Reserves are normally lower, and in this case, are estimated at 54%.

That’s it for today.

Every week we share our views on metals and mining stocks on socials and this blog. Subscribe here for highlights or see tools for vendors and junior miners below.

Before you go…

- Book a coaching session to discuss your mining project

- Get our step-by-step marketing framework for juniors and small caps, to grow faster

Synergy Resource Capital is a boutique investment and corporate advisory firm focused on natural resources and technology, and based in Sydney.

Disclaimer: Opinions and materials presented are not investment or financial advice and are intended for informational and educational purposes only; please consult a financial advisor before investing. Companies mentioned publicly may be held and/or clients, except within the member section. Content might contain affiliate links. By reading or sharing, you agree to our full disclaimer.

Investor, corporate? Join Synergy Resource Capital’s distribution list for our newsletter and updates.

I am heavily invested in 4CE – Force Commodities

LikeLiked by 1 person

Great to hear you’re in the sector!

LikeLike