This week’s commentary will be centered on one of our favourite commodities: copper. Last Friday, copper broke the USD 4 barrier for the first time since 2011, and today remains charging ahead in a move that has been widely anticipated by long-term supporters of the red metal. Copper is widely used in industry since the beginning of the 20th century, but these days its fundamental role in electrification and EV adoption undoubtedly promises to keep pushing, even higher than before.

LME inventories sit now on lows not seen since 2005 (according to Canaccord), and geopolitical stress and events in Chile (the world’s largest producer) as well as Peru and the US, promise to further deepen the situation.

However, in terms of fundamentals, we believe that copper supply has a wider challenge ahead. On one side, battery makers will be desperately wanting to secure raw materials for manufacturing ahead of an unprecedented demand in batteries (which some expect to cause a shortage in battery supply as well, such as QuantumScape, a partner of the VW Group), as electrification becomes mainstream. Secondly, this trend requires strengthening the existing charging network which would be the largest global infrastructure effort ever attempted by humanity. Hence demand will remain strong, for years to come. Finally, although slowed down, China’s urbanisation remains burgeoning.

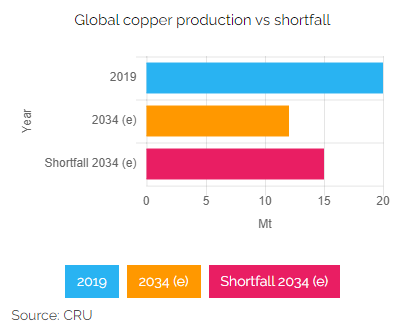

Now, on the supply side lies the problem. Copper deposits usually are large, extremely capital intensive, and located in remote areas, requiring significant investment in infrastructure of their own. In recent years, with entrenched volatility, investors have turned much more to gold projects which are closer to production and cash flow meaning the rate at which copper projects have turned into mines has slowed down. Commodities Research Unit (CRU) predicts global copper mined production will fall from 20Mt to below 12Mt by 2034, leading to a supply shortfall of more than 15Mt. Over 200 copper mines are expected to run out of ore before then, as reported by Mining.com last December.

There’s a decent lineup of copper deposits awaiting a financing decision, but many are located in jurisdictions with higher risk or longer permitting processes and have been delayed for years or even decades. Alas, to produce enough copper for all these requirements, we will need a shift in this dynamic and the allocation of massive pools of capital to build the new copper mines our future selves will need.

It’s always been you, copper…

And that is it for today. We’d love to hear your thoughts. Reach out on our social media channels and find additional resources here. See you next week!

The Weekly by Synergy: 5-minute musings on the markets, current trends, and events. From our opinions, observations, analysis, and news commentary, just a few lines to get you started every week.

Disclaimer: Our content is intended to be used for informational and educational purposes only. For more details, see our full disclaimer.