The ‘Goldman Sachs vs lithium’ saga is far from over.

Lithium stocks are bleeding everywhere.

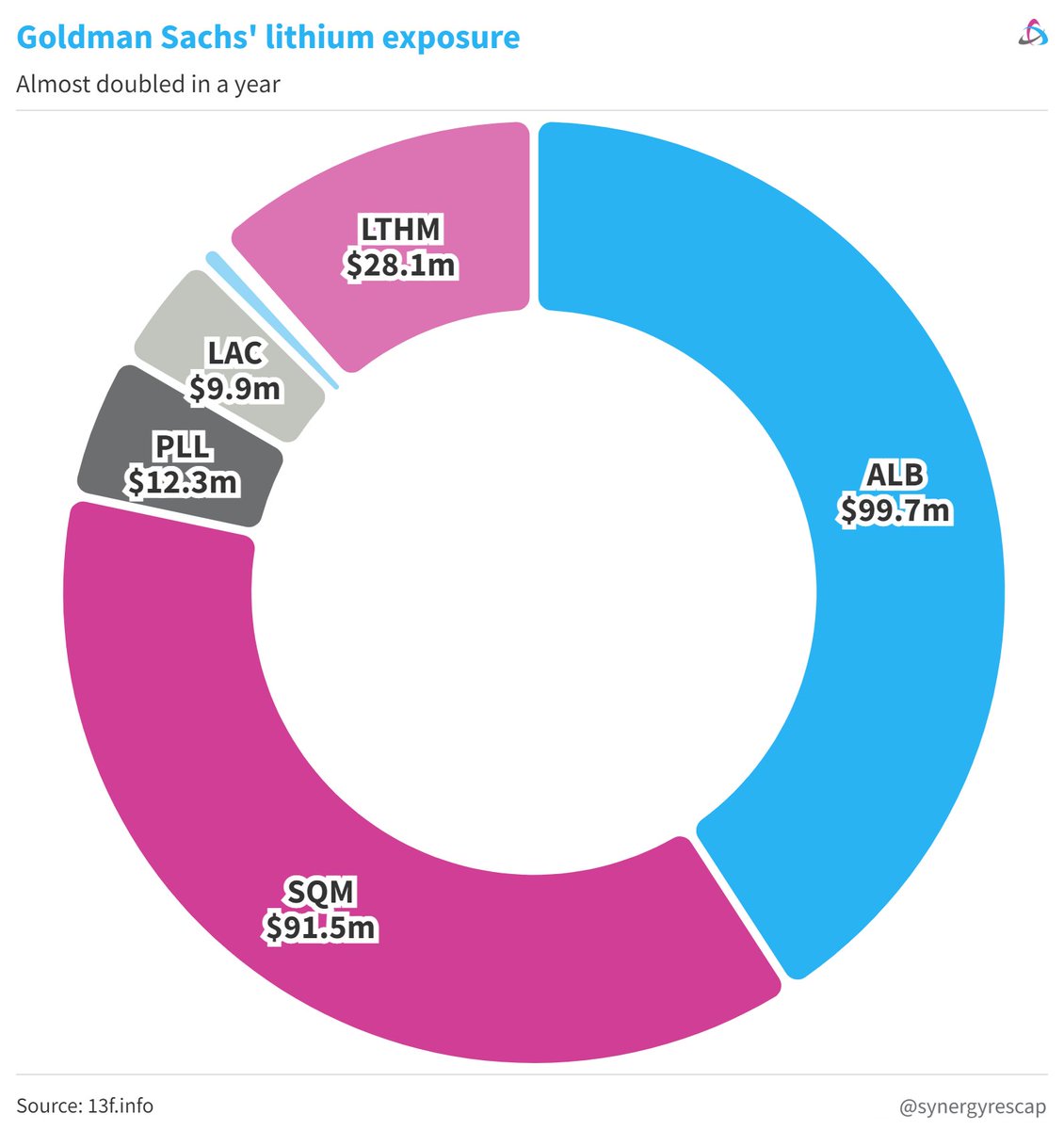

Yet GS’ lithium exposure has never been larger.

I went through their 13F filings and the most recent news since my November thread.

Here’s your update:

By the way…

I’ve been investing in lithium since 2008 so I’ve seen a couple of booms and valleys.

Also seen plenty of bulls and bears.

Reality is fundamentals have never been as strong as today.

So… I’m long the energy transition.

But let’s talk about Goldman Sachs.

First, let’s discuss price forecasts.

Goldman sees lithium carbonate falling to $53k/t in 2023, and plummeting to $11k in 2024.

For reference, current price is over $80k, and proving to be quite resilient despite the chatter.

(I’d say price listens to wallets, not words)

Other banks disagree, including:

-Macquarie

-JP Morgan (see my Nov thread link at the end)

-Citi

$MS says the consensus target price for 2024 is $29k, less than half today, but nearly triple GS’ estimate. Morgan Stanley are less bullish while also citing growing pains.

Lithium bulls are led by $MQG.

They see an average of $62k in 2023, to $72k until 2026 on a supply deficit.

‘Despite near-term price volatility, we believe buoyant lithium prices present potential for valuation upside to all our lithium names.’

$UBS sees strong demand in metals across the board, but also notes that:

“Lithium prices so far [have been] immune to macro weakness,”

And maintains ‘buy’ for $AKE $MIN

While Citi calls $40k in 2023, lukewarm $25k in 2024 (yet still great).

On the other hand, $GS also says they first called comm supercycle in 2020 and matches price spikes we’ve seen this year.

“Solving this problem [energy transition] requires large-scale capital investment and we’re not even close.”

Jeff is awesome. Be like Jeff.

📊 @markets

Additionally, Goldman cited China as one of the reasons for their bearish sentiment.

They then said this:

Australia’s lithium sector went from A$15b to A$60b in market cap value in 2 years.

It’s also the largest producer globally.

But expanding production is hard.

Even when you’re the leader.

In Aug Canaccord said:

‘Our forecast revisions see average YoY supply growth of 30% to 2025E, but in the short term, we don’t expect material new supply until early 2023.

Longer term, we expect supply growth of 285% to 2.3Mt LCE by 2030.’

(they cover heaps, inc $LAC)

But $CF also said:

‘timeline warrants some cynicism, due to:

-industry’s track record of project delays,

-rising capital intensities/financing risks,

-permitting & gov intervention risk

-technical risk/new process techs/

-“unconventional” Resources

(capacity ≠ market supply)’

Just a few days ago @FinancialReview reported on plenty of misses in production and delays in commissioning.

Yes, it happens often.

Benchmark also explained it well here (I summarised):

But let’s go back to Goldman for the ‘piece de resistance’.

Here’s the nugget.

$GS holds, according to their 13F as of Sep 30, 2022:

$ALB

$SQM

$LTHM

$PLL

$LAC

$SGML

$SLI

Their combined exposure went from $116m and 1.3m shares in 2021, to $244m, and 2.2m shares.

Who’s bearish?

Granted, these are only 7/6,254 holdings so to them it’s peanuts.

But still, twice as many peanuts!

Also note the lithium market was ~$5b in 2020 vs ~$950b combined iron, aluminum, copper & gold.

Oh, by the way, Goldman also initiated coverage on:

$CXO

$PLS

$LTR

$IGO

Call me crazy but I’ll believe their bear case when they reduce their allocation to the sector.

I don’t think it’ll happen.

But I promise I’ll track it.

I’ve seen many of these banks change tunes from

‘no lithium for us’ to ‘we love it’.

In the meantime, I remain bullish.

For more background, here’s what I wrote in mid-November in case you haven’t seen it.

(includes JP Morgan’s sentiment plus what several experts say)

That’s a wrap!

The saga is not over. Watch this space (literally).

If you enjoyed this…

- Invest more confidently with Mining Investing 101

- Become a member for weekly opportunity alerts and access to the whole vault

Or read the latest posts

Disclaimer: Opinions and materials presented are not investment or financial advice and are intended for informational and educational purposes only; please consult a financial advisor before investing. Companies mentioned publicly may be held and/or clients, except within the member section. Content might contain affiliate links. By reading or sharing, you agree to our full disclaimer.

Investor, corporate? Join Synergy Resource Capital’s distribution list for our newsletter and updates.