For decades, Chile has sat unchallenged at the top of global copper production. It isn’t a recent achievement or a cyclical spike — it’s a structural reality. In 2024 alone, Chile produced around 5.3 million tonnes of copper, comfortably ahead of every other producer on the planet. The Democratic Republic of Congo and Peru round out the podium, but Chile remains the benchmark.

These are absolute leaders. The countries every major miner, investor, and government watches when thinking about future of copper supply.

But here’s the thing.

The next chapter may require looking just a little bit east.

Argentina.

The country hasn’t earned a place on that podium, as its only copper mine, Alumbrera, was shut down in 2018 after exhausting reserves.

But the absence is becoming increasingly misleading.

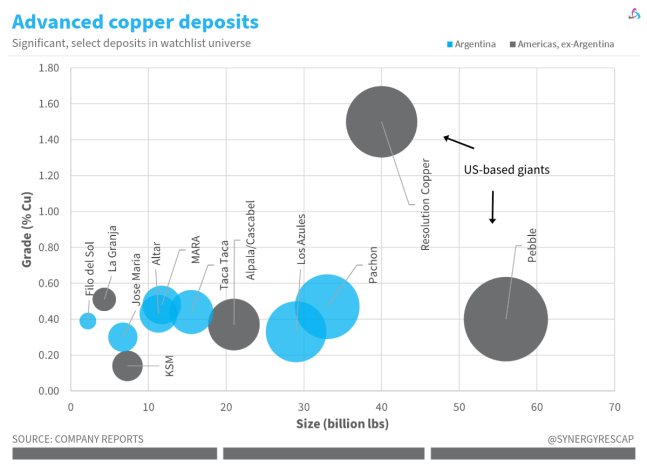

Stretching more than 5,000 kilometres, the border between Chile and Argentina cuts straight through the Andes — one of the most copper‑endowed mountain belts on Earth. Geology, after all, doesn’t recognise borders. The same magmatic systems that host Chile’s world‑class porphyries continue across the frontier, where Argentina hosts a growing pipeline of large, advanced copper projects.

For years, those projects have been stuck in a holding pattern. Not because of geology. Not because of scale. But because of uncertainty — regulatory, fiscal, political, and economic. Capital at this level doesn’t tolerate ambiguity, and Argentina has historically supplied too much of it.

That is now changing.

Under President Javier Milei, Argentina is signalling a decisive shift toward market‑friendly policies, fiscal discipline, and a clearer framework for foreign investment. Whether one agrees with his politics or not, the direction of travel is unmistakable: certainty is becoming a policy goal.

And for copper, certainty matters.

I know you’re thinking. Will it work this time?

It is a fair question. After all, Argentina’s track record has been abysmal. So much so that many investors swore to stay away.

I’ll tell you my 2 cents.

Several major deposits along the Andes, at the border between the two countries—many already discovered, drilled, and technically de‑risked—don’t need higher copper prices to work. They need predictability. Stable rules. Confidence that long‑dated capital won’t be punished mid‑cycle. I personally worked and even visited several of them.

If Argentina delivers that, the country doesn’t need to rival Chile overnight to matter. It simply needs to move. Even one or two large projects entering construction would alter perceptions — and eventually, supply forecasts.

RIGI, a new incentive regimen, is the latest evidence of this shift.

So, while Chile’s dominance remains unquestioned, the smart money is starting to scan the horizon.

Argentina may not be on the chart yet. But the geology is there. The projects are there.

And for the first time in ages, the conditions to unlock them might be too.

Latest posts

- Houston, we have a (duration) problem

- This is where copper is going (and fast!), according to BHP & Rio Tinto

If you enjoyed this…

- Become a member to access all toolkit topics and research

- Get started with the eBook, Mining Investing 101

Disclaimer: Opinions and materials presented are not investment or financial advice and are intended for informational and educational purposes only; please consult a financial advisor before investing. Companies mentioned publicly may be held and/or clients, except within the member section. Content might contain affiliate links. By reading or sharing, you agree to our full disclaimer.

Investor, corporate? Join Synergy Resource Capital’s distribution list for our newsletter and updates.

Sources: Canaccord research, Bloomberg, Reuters, Mining.com, TradingView, ASX, TMX, NASDAQ, LSE and SRC research. Figures shown in US dollars unless clarified.